What does declining balance depreciation on buildings mean?

Under the Growth Opportunities Act, since 2023, capital investors have been able to choose between straight-line depreciation and the newly introduced declining balance depreciation on buildings for wear and tear (Section 7 (5a) of the German Income Tax Act (EStG)) for new rental apartment buildings under certain conditions.

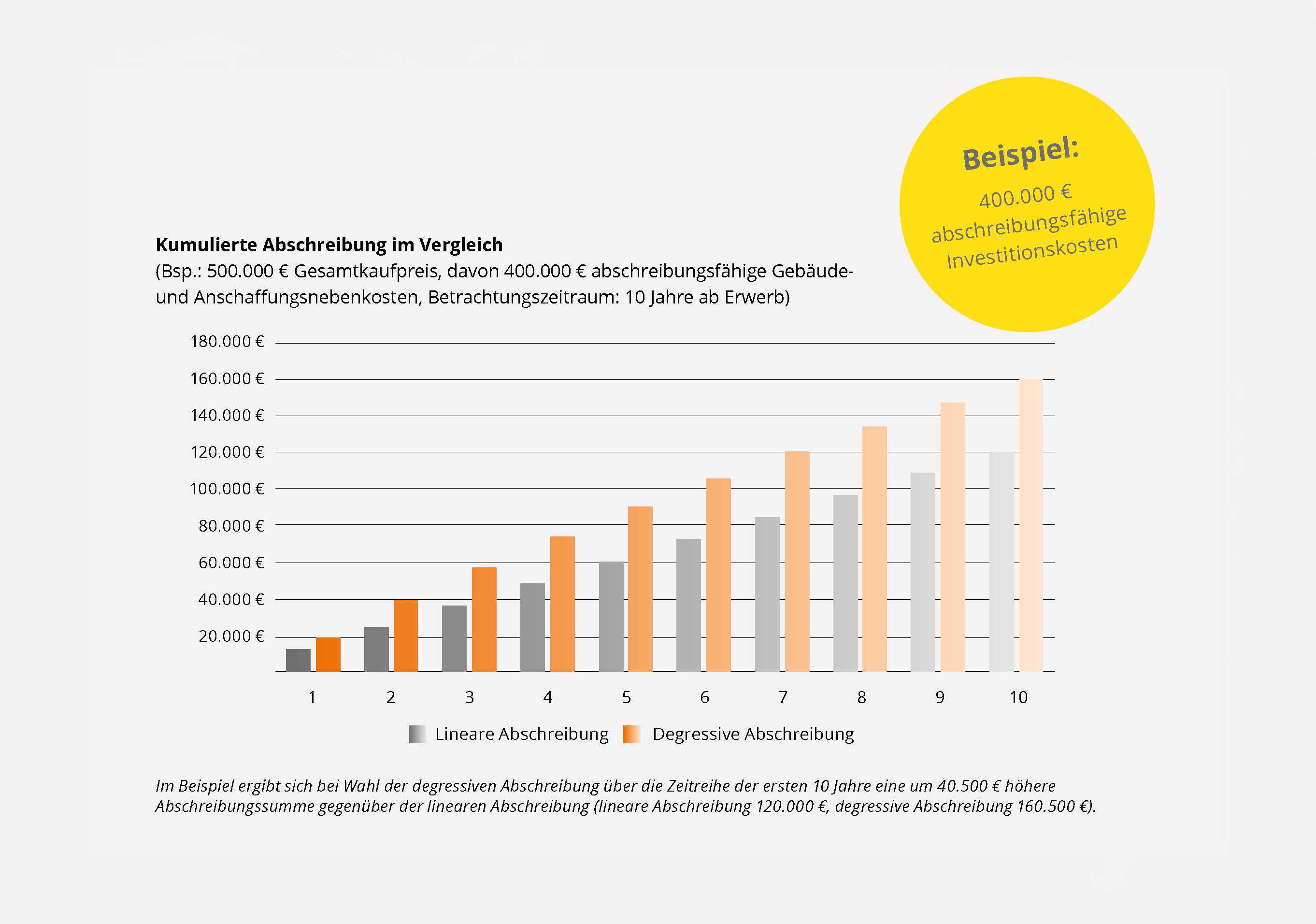

The declining balance method of building depreciation allows for a disproportionate deduction of the depreciable acquisition costs (building portion plus proportionate ancillary costs of the purchase price) in the early years of the investment, whereas with straight-line depreciation, the tax deduction is distributed evenly over the useful life of the property.

Declining balance depreciation: 5% of the depreciable residual book values p.a. (later change to straight-line depreciation possible). Straight-line depreciation: 3% of the depreciable investment costs p.a. over 33.3 years.

This results in the following potential advantages:

- Offsetting of building depreciation against other income of the capital investor

- Option of tax-optimized distribution of depreciation

- possible liquidation advantage as a result

Talk to your tax advisor about this!